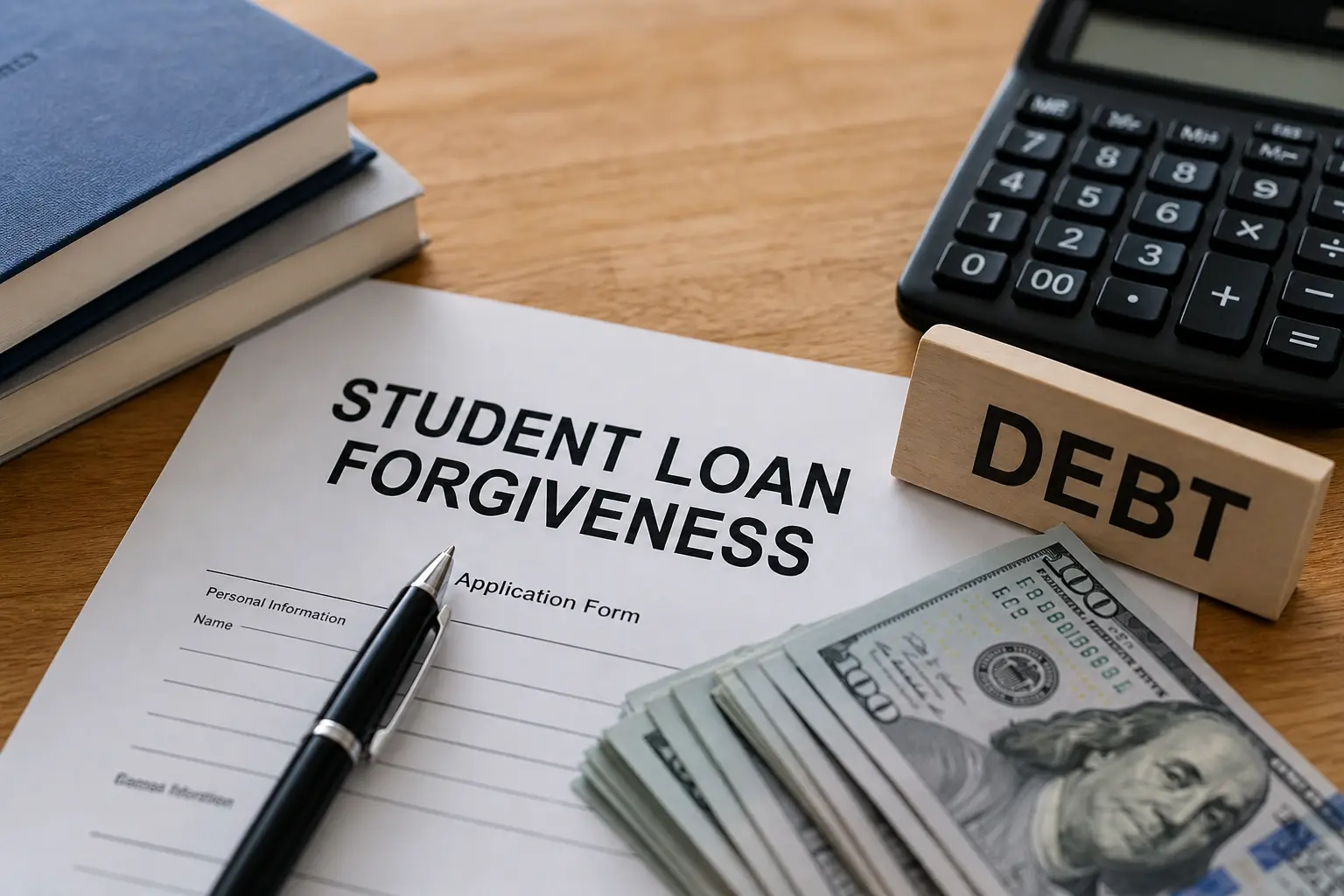

You finally got student loan forgiveness. Then the IRS showed up.

After years of payments, delays, and political promises, millions of borrowers thought relief was finally here. But in 2026, a painful reality is returning: forgiven student loans may once again be treated as taxable income at the federal level.

Nobody told you this part.

For borrowers already struggling with rent, inflation, and rising living costs, this changes everything. And if you live in California, Texas, or New York — states carrying some of the highest student debt burdens in America — the impact could hit even harder.

What looked like financial freedom may come with another bill waiting behind it.

Main Explanation

During the pandemic years, the federal government temporarily made student loan forgiveness tax-free under the American Rescue Plan. For many borrowers, it felt like the first real break in years.

That protection is ending.

Starting in 2026, forgiven balances under several student debt forgiveness programs could again count as ordinary income under federal tax rules. In simple terms, if $20,000 of your student debt disappears, the IRS may treat that amount as money you earned.

And earned income gets taxed.

For many middle-income borrowers, that could create a surprise tax bill between $2,000 and $5,000. In larger forgiveness cases, the number could climb much higher.

The timing makes this worse. Student loan forgiveness programs have expanded rapidly over the last few years. More Americans are entering Income-Driven Repayment plans, Public Service Loan Forgiveness programs, and state-level debt relief systems than ever before.

Ten years ago, student loan forgiveness felt like a political talking point. Today, it affects millions of real people trying to survive financially.

But the rules keep changing mid-game.

Impact

The people most affected are not wealthy borrowers with large savings accounts. They are teachers, nurses, public workers, and middle-class graduates already stretched thin.

A borrower receiving $30,000 in forgiveness while sitting in a 22% federal tax bracket could suddenly owe roughly $6,600 to the IRS.

That is not a small inconvenience.

That is rent money. Emergency savings. Grocery money. Childcare money.

Imagine finally escaping years of debt only to open another bill months later.

This is where relief turns into panic.

Borrowers in California, Texas, and New York face different outcomes depending on state tax rules. Texas has no state income tax, meaning federal taxation becomes the main burden. New York often aligns closely with federal tax policy. California may treat forgiven debt differently at the state level, creating even more confusion for borrowers trying to plan ahead.

Same forgiveness. Completely different financial outcomes depending on your zip code.

And that uncertainty creates another kind of pressure people rarely talk about: mental exhaustion.

Many borrowers already feel trapped by constantly changing repayment plans, court battles, and shifting federal announcements. Every new update forces people to rethink their finances again.

People do not panic because of events. They panic because of uncertainty.

Insight

The uncomfortable truth is simple: forgiveness without financial education can become a delayed crisis.

Many borrowers will celebrate loan cancellation in 2026 without fully understanding the federal student loan tax 2026 consequences attached to it. Months later, tax season could deliver a brutal surprise.

The system itself also exposes a deeper problem. Student loan policies now shift with elections, court decisions, and economic pressure. What is true one year may completely change the next.

That instability punishes the people least prepared to adapt.

A decade ago, most borrowers worried about whether forgiveness would ever happen. Now the fear is different. People worry about what hidden cost comes after the forgiveness arrives.

And there is another growing divide: informed borrowers versus uninformed borrowers.

The borrowers who understand tax consequences, repayment structures, and policy changes early often protect themselves better. Everyone else risks learning too late.

That gap is growing fast.

Conclusion

Student loan forgiveness 2026 is real. But so is the financial risk attached to it.

For borrowers in California, Texas, and New York, the return of taxable forgiveness could create a second wave of financial pressure just when relief finally seemed close.

Before celebrating cancellation notices, borrowers need to understand the full cost of what comes next.

Because forgiveness that comes with a surprise bill is not freedom.

It is just a different kind of debt.

You finally got student loan forgiveness. Then the IRS showed up.

After years of payments, delays, and political promises, millions of borrowers thought relief was finally here. But in 2026, a painful reality is returning: forgiven student loans may once again be treated as taxable income at the federal level.

Nobody told you this part.

For borrowers already struggling with rent, inflation, and rising living costs, this changes everything. And if you live in California, Texas, or New York — states carrying some of the highest student debt burdens in America — the impact could hit even harder.

What looked like financial freedom may come with another bill waiting behind it.

Main Explanation

During the pandemic years, the federal government temporarily made student loan forgiveness tax-free under the American Rescue Plan. For many borrowers, it felt like the first real break in years.

That protection is ending.

Starting in 2026, forgiven balances under several student debt forgiveness programs could again count as ordinary income under federal tax rules. In simple terms, if $20,000 of your student debt disappears, the IRS may treat that amount as money you earned.

And earned income gets taxed.

For many middle-income borrowers, that could create a surprise tax bill between $2,000 and $5,000. In larger forgiveness cases, the number could climb much higher.

The timing makes this worse. Student loan forgiveness programs have expanded rapidly over the last few years. More Americans are entering Income-Driven Repayment plans, Public Service Loan Forgiveness programs, and state-level debt relief systems than ever before.

Ten years ago, student loan forgiveness felt like a political talking point. Today, it affects millions of real people trying to survive financially.

But the rules keep changing mid-game.

Impact

The people most affected are not wealthy borrowers with large savings accounts. They are teachers, nurses, public workers, and middle-class graduates already stretched thin.

A borrower receiving $30,000 in forgiveness while sitting in a 22% federal tax bracket could suddenly owe roughly $6,600 to the IRS.

That is not a small inconvenience.

That is rent money. Emergency savings. Grocery money. Childcare money.

Imagine finally escaping years of debt only to open another bill months later.

This is where relief turns into panic.

Borrowers in California, Texas, and New York face different outcomes depending on state tax rules. Texas has no state income tax, meaning federal taxation becomes the main burden. New York often aligns closely with federal tax policy. California may treat forgiven debt differently at the state level, creating even more confusion for borrowers trying to plan ahead.

Same forgiveness. Completely different financial outcomes depending on your zip code.

And that uncertainty creates another kind of pressure people rarely talk about: mental exhaustion.

Many borrowers already feel trapped by constantly changing repayment plans, court battles, and shifting federal announcements. Every new update forces people to rethink their finances again.

People do not panic because of events. They panic because of uncertainty.

Insight

The uncomfortable truth is simple: forgiveness without financial education can become a delayed crisis.

Many borrowers will celebrate loan cancellation in 2026 without fully understanding the federal student loan tax 2026 consequences attached to it. Months later, tax season could deliver a brutal surprise.

The system itself also exposes a deeper problem. Student loan policies now shift with elections, court decisions, and economic pressure. What is true one year may completely change the next.

That instability punishes the people least prepared to adapt.

A decade ago, most borrowers worried about whether forgiveness would ever happen. Now the fear is different. People worry about what hidden cost comes after the forgiveness arrives.

And there is another growing divide: informed borrowers versus uninformed borrowers.

The borrowers who understand tax consequences, repayment structures, and policy changes early often protect themselves better. Everyone else risks learning too late.

That gap is growing fast.

Conclusion

Student loan forgiveness 2026 is real. But so is the financial risk attached to it.

For borrowers in California, Texas, and New York, the return of taxable forgiveness could create a second wave of financial pressure just when relief finally seemed close.

Before celebrating cancellation notices, borrowers need to understand the full cost of what comes next.

Because forgiveness that comes with a surprise bill is not freedom.

It is just a different kind of debt.